Trump Accounts: What To Know Right Now

A new federal law just created a child investment account with a $1,000 government head start. Here's the plain-language breakdown, and how it fits into a real financial plan.

If you have kids, or are planning to, there's a new account type on the table worth knowing about. As of July 2025, Congress passed the One Big Beautiful Bill Act, which added IRC Section 530A to the tax code and created what are officially called "Trump Accounts." Regardless of where you land politically, the mechanics here are real and worth understanding.

Let's break it down.

Why This Exists — And Why It Matters

The policy motivation behind Section 530A is straightforward. Surveys consistently show that a significant portion of Americans reach adulthood without meaningful retirement savings. Most retirement planning begins at first job, first 401(k) enrollment, often in someone's late 20s or 30s. That's a decade or more of compounding time already gone.

Congress created Trump Accounts to shift that timeline earlier, to birth, in some cases. For families thinking about multigenerational wealth, these accounts introduce a new planning tool that allows retirement saving to begin long before a child has earned income, while still preserving the long-term retirement character of the account. For advisors and their clients focused on family and legacy planning, that's a meaningful shift.

So, What Exactly Is It?

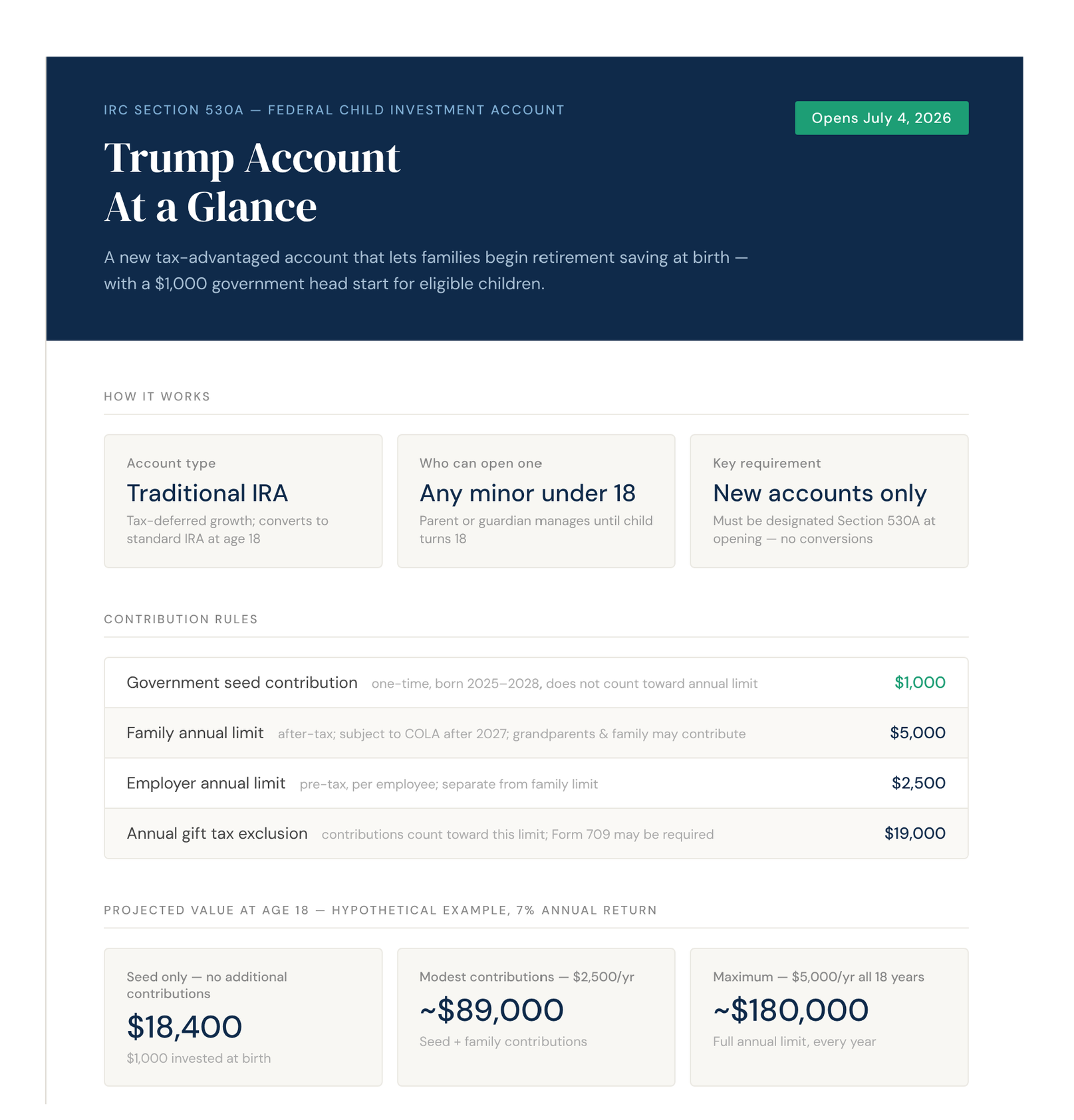

At its core, a Trump Account is a traditional IRA, but for minors. It's a federally structured investment account opened in a child's name, managed by a parent or guardian until the child turns 18. Think of it as a long runway for tax-deferred growth, starting at birth.

A few things make it structurally distinct from a standard IRA. The account must be formally designated as a Section 530A Trump Account at establishment, meaning the written governing instrument has to reflect the specific requirements of the statute. Trustees and custodians are responsible for ensuring compliance. And critically: an existing IRA cannot be converted or retroactively amended into a Trump Account. The designation has to happen when the account is first opened. If you're thinking of applying this to an account you've already set up for your child elsewhere, that's not permitted under the current rules.

The IRS formally opened these accounts on July 4, 2026, the 250th anniversary of the Declaration of Independence. It's a stock market index investment account, not a savings account, so the money is designed to grow over time in the market.

The $1,000 From the Government — Here's The Fine Print

For children born between January 1, 2025 and December 31, 2028, the federal government will deposit a one-time $1,000 "seed" contribution into their Trump Account. This is called the pilot program contribution, and crucially, it does not count against the annual contribution limit.

That's free money, but only if you take action and open the account. It doesn't happen automatically.

The Contribution Rules, Laid Out Simply:

Government seed = $1,000. For kids born 2025–2028

Family annual limit = $5,000. Subject to cost-of-living adjustments after 2027

Employer limit = $2,500. Per employee per year, tax-free at federal level

Family contributions, from you, grandparents, aunts and uncles, close family friends, are made with after-tax dollars and count toward the $5,000 annual limit. They're non-deductible, meaning you won't get a tax break going in, but growth inside the account is tax-deferred. You pay taxes when money comes out, not while it compounds.

This is where the multigenerational angle gets interesting. Grandparents who want to leave a financial legacy but aren't sure how to structure it now have a purpose-built vehicle. It's not a trust, it's not a 529, it's a retirement account seeded in childhood, with decades of runway ahead of it.

The "Growth Period" — And Why It Matters

The account operates under special rules from the day it's opened until December 31 of the year the child turns 17. During this "growth period," there are no required minimum distributions, and the money is locked in, no early withdrawals. At 18, the account rolls into a traditional IRA and is treated accordingly from that point forward.

For a client in the 35–50 range with a young child, this is essentially a forced long-term investment with a multi-decade compounding runway. A child born in 2025 who has this account invested in a broad index fund for 18+ years has time squarely on their side, and that's before factoring in what they continue to contribute as an adult.

What It's Not — And Where To Be Careful

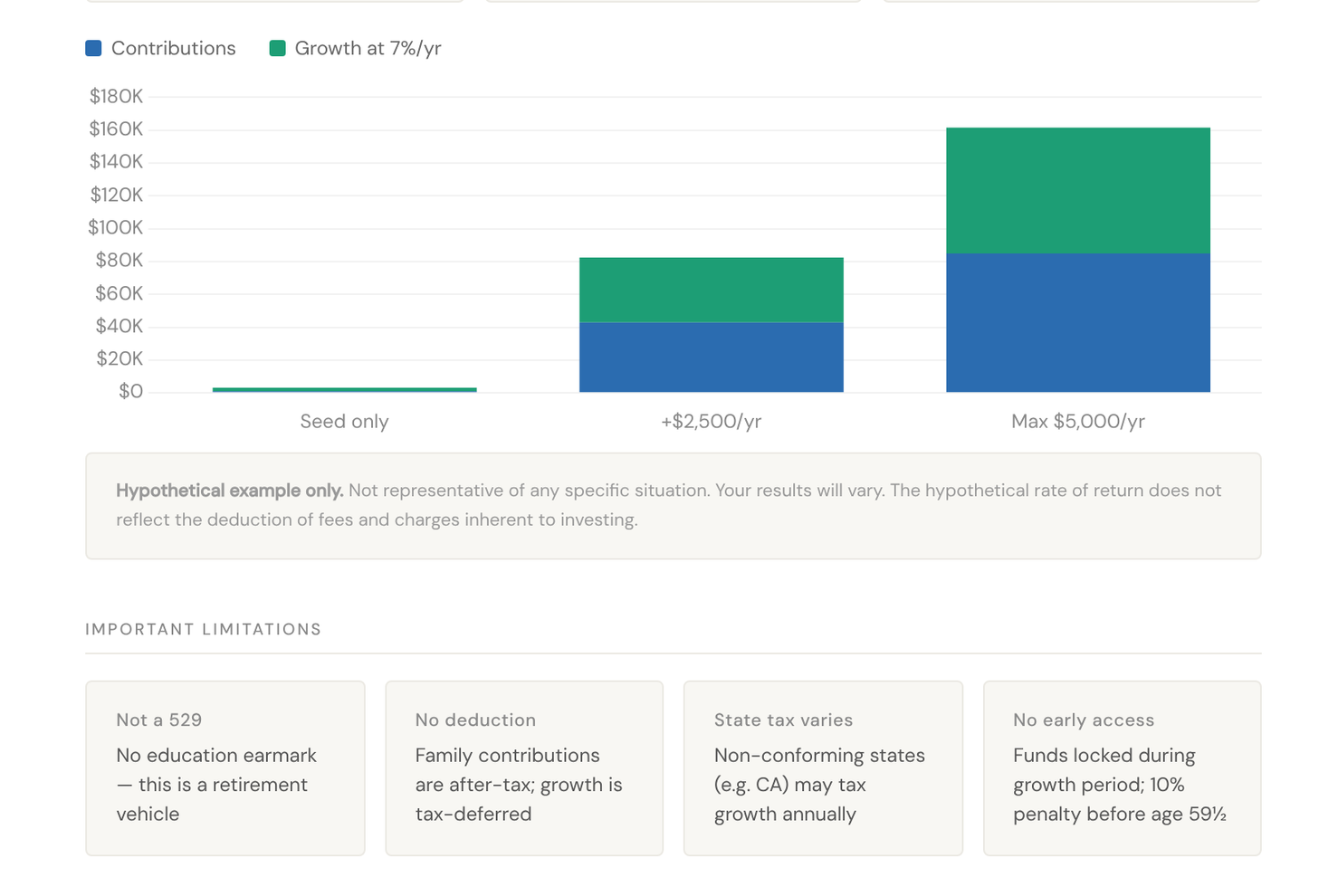

It's not a 529. A 529 is earmarked for education expenses. This account has no such restriction, it's a retirement account at the end of the day. If you're prioritizing college savings, don't confuse the two.

Contributions aren't deductible. Unlike a traditional IRA for adults, you put in after-tax money. This limits one of the classic IRA advantages.

You can't convert an existing account. If you already have a custodial or IRA-style account set up for your child, it cannot be retroactively redesignated as a Trump Account. The Section 530A designation must be made at account opening, full stop.

State tax treatment varies. States aren't required to follow federal rules. California, for example, currently does not conform. If you live in a non-conforming state, your state may tax investment growth annually, undercutting the tax-deferred benefit.

Gift Tax: A Nuance Worth Flagging

Because your child doesn't have immediate access to the funds, contributions may require filing a gift tax return (Form 709). The $5,000 annual cap does count toward the annual gift exclusion limit — currently $19,000 — so if grandparents or other family members are contributing, plan your broader gifting strategy accordingly. This is exactly the kind of coordination a financial advisor should be helping you think through.

The Power of Starting Early: What Compounding Actually Looks Like

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rate of return used does not reflect the deduction of fees and charges inherent to investing.

One of the strongest arguments for opening a Trump Account is simple math. A child born in 2025 who receives the $1,000 government seed and has that money invested in a broad U.S. index fund for 18 years — at a historically conservative 7% annual return — could have over $18,000 by the time they turn 18, without a single additional dollar contributed. Add modest family contributions of $2,000–$3,000 per year, and that number climbs well past $60,000–$80,000. Max out the $5,000 annual limit for all 18 years, and the account could exceed $180,000 — handed to a young adult at exactly the age when most people have nothing saved. The earlier the account is opened and funded, the more time compounds in your child's favor.

The numbers above may illustrate how significant early contributions can be in some cases.

This isn't a magic solution. It has real limitations compared to other vehicles. But the government seed money, the long growth runway, and the ability to involve extended family in contributing all make it a legitimate addition to a family financial plan, particularly for clients who are already thinking about how wealth flows across generations.

What To Do Next

Final regulations are still being written, so some details may evolve through the rest of 2026. What we know now is enough to start planning. A few immediate steps worth taking:

If you have a child born in 2025–2028, look into electing the pilot program contribution, accounts opened starting July 4, 2026 qualify for the $1,000 government deposit.

Review how this fits alongside any existing 529, custodial account (UGMA/UTMA), or Roth IRA strategy already in place for your family.

Check your state's tax conformity, this matters more than most people realize and could affect the net benefit of the account significantly.

If grandparents or other family members want to contribute, loop in your advisor to coordinate gifting strategy and any Form 709 filing requirements.

If your employer offers this as a benefit, understand the $2,500 annual limit and how it interacts with the family contribution cap.

Have questions about how a Trump Account fits into your family's financial picture?

We would be happy to walk through your particular situation, from first-time parents to grandparents thinking about legacy. Regulations are still developing, but the planning conversation is worth having today.

Please note, Trump Accounts offer tax deferred growth on earnings and provide tax free withdrawals when distributions are qualified. Contributions may include after tax family contributions, pre tax employer contributions, and a one time $1,000 federal contribution for eligible children born between 2025 and 2028. Under current tax law, withdrawals prior to age 59½ may result in a 10% IRS penalty tax, in addition to current income tax, and may be restricted until the child reaches age 18. Annual contribution limits and other restrictions apply. Some Trump Account rules and regulations are still forthcoming from the U.S. Treasury and IRS. Clients should consult with a qualified tax advisor or financial professional before making any decisions.

The opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual. The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.