Exploring the Different Retirement Accounts for Business Owners

Retirement planning is a crucial aspect of financial management, and for business owners, it requires careful consideration of many different factors. Business owners have the unique advantage of utilizing specialized retirement accounts that can significantly boost their retirement savings while providing valuable tax advantages. In this blog post, we will delve into the different retirement accounts available to business owners, highlighting their features, benefits, and eligibility requirements. By understanding these options, business owners can make informed decisions to secure a prosperous retirement.

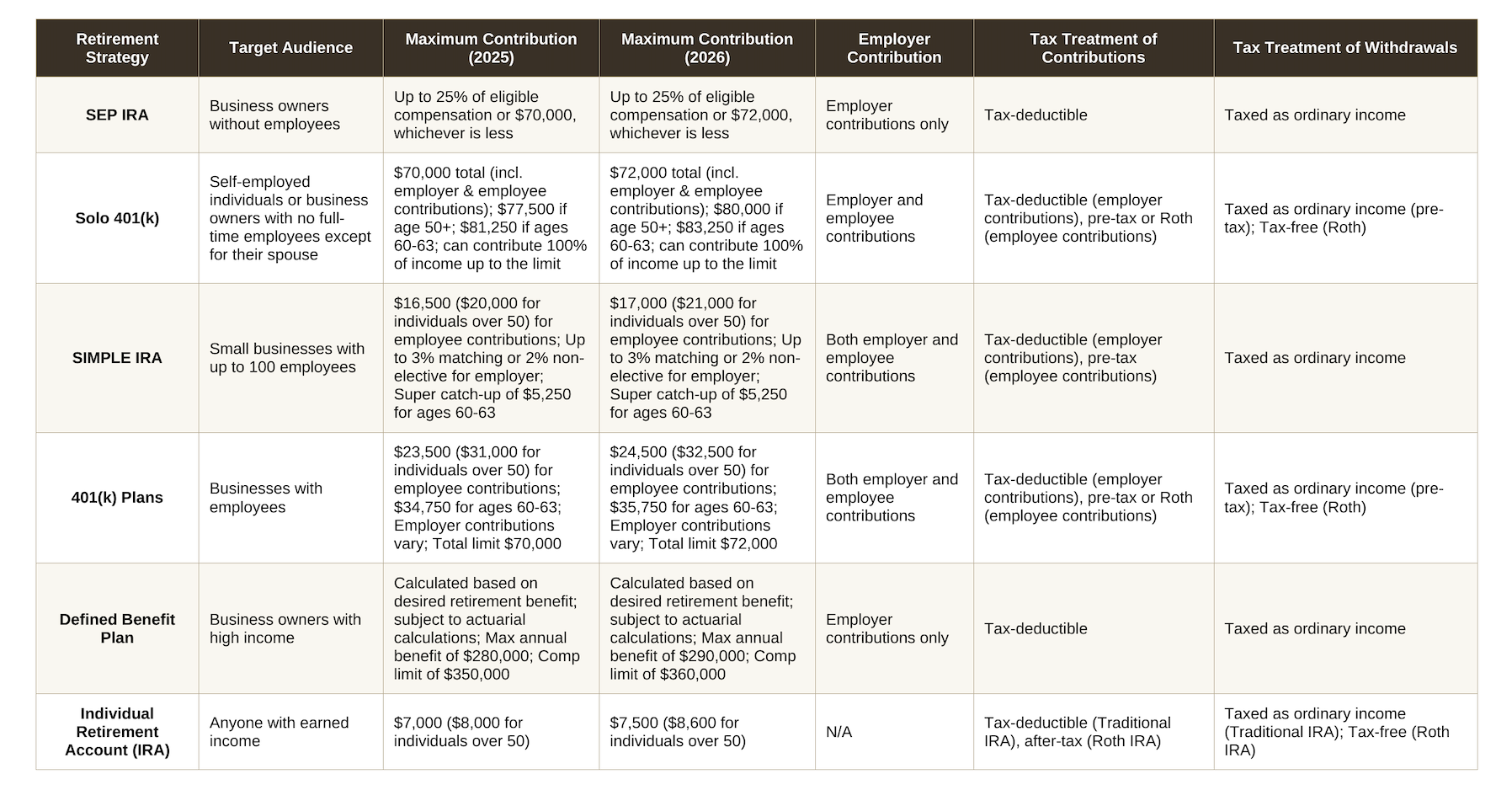

1. Simplified Employee Pension (SEP) IRA:

The Simplified Employee Pension (SEP) IRA is a popular retirement account choice for business owners, particularly those with no employees. SEP IRAs are easy to set up and maintain, offering significant contribution limits. Business owners can contribute, and fully deduct, up to 25% of their eligible compensation (or a maximum of $72,000 in 2026) to their SEP IRA. Contributions are tax-deductible, and the earnings grow tax-deferred until withdrawal during retirement.

Consider this example: If you are a business owner earning $100,000 per year and you were able to contribute 25% of your income to your SEP IRA, you immediately reduce your taxable income to $75,000. This means that your Federal tax bill just went from $16,712 to $11,212 saving you $5,500 (using 2026 single tax rates). If you are an LLC or Sole Proprietor, you also owe self-employment tax but your contribution to your SEP IRA just reduced your tax bill from $15,300 to $11,475 saving you $3,825. In this example, you just saved $9,325 and we haven’t even factored in any state tax savings!

Keep in Mind: A SEP IRA might not be the best choice for you if you have employees. With a SEP IRA, you are required to contribute equal percentage amounts to every employee of your business, including yourself.

2. Solo 401(k):

Also known as an Individual 401(k) or Self-Employed 401(k), the Solo 401(k) is designed for self-employed individuals or business owners with no full-time employees, except for their spouse. The total contribution limit is $72,000, including both employer and employee contributions, for 2026. The employee deferral limit is $24,500 for 2026. However, you can contribute 100% of your income up to the employee deferral limit in a Solo 401(k). This means that if your business made $72,000, you could contribute the entire amount (combining employee and employer contributions) into a Solo 401(k) and not pay any taxes! Obviously, this would only work if you had other sources of income to live off of but a lot of entrepreneurs start their business as a side hustle so this can certainly be a great option!

You are also permitted to make catch-up contributions in a Solo 401(k), as opposed to the SEP IRA, which means you can contribute an additional $8,000 if you are age 50 to 59 or 64 and older. Thanks to the SECURE 2.0 Act, if you are between the ages of 60 and 63, you can make an enhanced “super catch-up” contribution of $11,250 instead of the standard $8,000, bringing your potential total contribution even higher.

New for 2026: If your prior-year W-2 wages exceeded $150,000, you are now required to make catch-up contributions on a Roth (after-tax) basis. Make sure your plan documents support Roth deferrals to continue making catch-up contributions.

3. SIMPLE IRA:

A Savings Incentive Match Plan for Employees (SIMPLE) IRA is an attractive retirement plan option for small businesses with up to 100 employees. It provides a straightforward and cost-effective way for employers to offer retirement benefits to their employees while saving for their own retirement.

With a SIMPLE IRA you, as the business owner, can contribute both as an employee and as the employer.

The maximum SIMPLE IRA employee contribution limit is $17,000 in 2026. Employees who are 50 or older are also eligible to make additional catch-up contributions up to $4,000 if their SIMPLE IRA plan permits it. That means you or any employees who are 50 or older could contribute a maximum of $21,000 in 2026. Additionally, the SECURE 2.0 Act introduced a “super catch-up” for participants aged 60 to 63, allowing an additional $5,250 in catch-up contributions.

Employees who contribute to any other employer plans with elective salary reductions are also subject to an aggregate limit of $24,500 in 2026. In other words, if you have both a 401(k) and a SIMPLE IRA, you can only contribute a maximum of $24,500 across both accounts. However, if you are 50 or older, catch-up contributions allow you to contribute up to an aggregate limit of $32,500 in 2026.

Employers can either:

Match their employees' contributions dollar-for-dollar up to a maximum of 3% of each employee's salary without any limit.

Make a contribution of 2% of each employee's salary (using only the first of $360,000 of salary in 2026) regardless of whether the employee makes contributions or not.

Employers who opt for matching contributions are allowed to reduce the match below 3%. However, it must be at least 1%, and they can reduce the match for no more than two out of five years.

Note for small businesses: Under SECURE 2.0, employers with 25 or fewer employees may qualify for higher contribution limits—up to $18,100 in employee deferrals for 2026. Check with your plan administrator to see if your plan is eligible.

4. 401(k) Plans:

401(k) plans are widely recognized retirement savings vehicles and they offer unique benefits for businesses that have employees. A 401(k) plan allows both the employer and employees to contribute to the retirement account, fostering a sense of employee engagement and loyalty. As a business owner, offering a 401(k) plan can help attract and retain talented employees.

For 2026, the 401(k) employee contribution limit is $24,500, or $32,500 if you are age 50 or older. Participants aged 60 to 63 can take advantage of the SECURE 2.0 “super catch-up” and contribute up to $35,750. The combined employee and employer contribution limit is $72,000 for 2026. Additionally, employers can choose to match a portion of employee contributions, which can further enhance the retirement savings for both parties.

One advantage of 401(k) plans is the availability of Roth 401(k) options. Similar to Roth IRAs, Roth 401(k) contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free, including any earnings. This option can be beneficial for business owners who anticipate being in a higher tax bracket during retirement or prefer tax-free income.

Important update for 2026: Starting in 2026, employees age 50 and older who earned more than $150,000 in W-2 wages from the prior year must make their catch-up contributions on a Roth basis. If your plan does not currently offer Roth contributions, higher earners may be unable to make any catch-up contributions once this rule takes effect.

Business owners should be aware that implementing a 401(k) plan comes with certain administrative responsibilities, including plan setup, recordkeeping, and compliance with applicable regulations such as nondiscrimination testing. Working with a retirement plan provider or a financial advisor specializing in retirement plans can help simplify the process and ensure compliance.

It’s important to note that business owners with employees may have additional fiduciary responsibilities as plan sponsors. Understanding these responsibilities and seeking professional guidance can help mitigate potential risks and ensure that the plan is managed in the best interest of the participants.

5. Defined Benefit Plan:

A Defined Benefit Plan, commonly known as a pension plan, offers significant retirement savings potential for business owners with a high income. Unlike other retirement accounts, the contribution limits for Defined Benefit Plans are calculated based on the desired retirement benefit. As a business owner, you can determine the annual contributions required to achieve a specific retirement benefit, subject to certain limits and actuarial calculations. While these plans require more administrative responsibilities, they can result in substantial tax deductions and generous retirement income.

6. Individual Retirement Account (IRA):

While not exclusive to business owners, one of the simplest retirement planning options available is to contribute to an Individual Retirement Account (IRA). IRAs are available to anyone with earned income and allow contributions up to $7,500 per year, or $8,600 per year for individuals 50 and older, if their modified adjusted gross income falls within the eligibility limits.

There are two types of IRAs: Traditional and Roth. Traditional IRA contributions are tax-deductible, and taxes are deferred until withdrawals are made. Contributions to a Roth IRA are made with after-tax dollars, meaning they do not provide immediate tax deductions. However, the withdrawals in retirement are generally tax-free, including any earnings generated over time.

Make it stand out

Whatever it is, the way you tell your story online can make all the difference.

As a business owner, exploring the various retirement account options is crucial for maximizing retirement savings while considering tax advantages, employee benefits, and administrative requirements. Choosing the most suitable retirement account(s) depends on factors such as the size of your business, employee count, desired contribution limits, and long-term retirement goals.

At Infinite Heights Wealth Management, we specialize in helping business owners navigate the complexities of retirement planning. We can assist you in selecting retirement accounts that align with your unique circumstances and provide comprehensive guidance throughout the process.

Remember, retirement planning is a long-term endeavor, and regularly reviewing and adjusting your strategy is essential to ensure you’re on track to achieve your retirement goals. Take proactive steps today to secure a financially independent and fulfilling retirement tomorrow.

The opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual.